Private equity in France now occupies a central role in corporate financing, the transformation of the economic fabric, and the generation of long-term value. As Europe’s second-largest private equity market, France combines market depth, strategic sophistication, managerial excellence among asset managers, and strong international capital appeal.

In an environment shaped by higher interest rates, strategic sovereignty considerations, the ecological transition and the digitalisation of business models, French private equity has demonstrated resilience. Net performance remains robust over the long term, while the economic footprint is meaningful: 2.5 million employees within backed companies and a cumulative €500 billion in combined revenues1.

Discover how to structure an allocation to institutional-grade French private equity via the Private Corner platform.

The French private equity market: key figures and momentum

France: Europe’s second-largest private equity market

French private equity ranks second in Europe by invested volumes.

This position rests on:

- A dense base of industrial SMEs and mid-sized companies (ETIs)

- A strong entrepreneurial culture

- Specialised and highly professional asset managers

- A stabilised regulatory environment

Consolidated data indicate:

- €36.9bn invested in 2024 (excluding infrastructure)

- 2,759 companies backed during the year

- 11,142 portfolio companies as of end-2024

French private equity is therefore a major channel for financing the real economy, with a material contribution to employment, innovation and the growth of SMEs and mid-sized businesses.

Approximately 35% of capital raised originates from international investors, underscoring the market’s attractiveness.

Key figures – French private equity (2024 – H1 2025)

| Indicator | Figure |

|---|---|

| Annual investments (excluding infrastructure) | €36.9bn |

| Portfolio companies | 11,142 |

| Jobs supported | 2.5 million |

| Net job creation in 2024 | +78,485 |

| Net IRR over 10 years | 12.4% |

| Private debt investments (2024) | €11.6bn |

| Infrastructure fundraising (2024) | €13.7bn |

These figures illustrate the maturity and depth of the French private equity market, which has become a structuring lever for the financing of SMEs, mid-sized businesses and strategic companies.

How French private equity has evolved in recent years

Despite a more demanding macroeconomic backdrop in 2023, French private equity retains strong fundamentals.

Net performance as of end-2024 remains elevated:

- 12.4% net IRR over 10 years

- 11.3% net since inception

- 14.1% for recently liquidated funds

Historically, French private equity has outperformed major listed asset classes over long horizons.

Economic impact

In 2024:

- +4.6% revenue growth across backed companies

- +78,485 jobs created

- +530,000 additional jobs over five years

Private equity is therefore not merely a vehicle for financial performance: it also constitutes a structural driver of the French economy’s development.

Private equity strategies most favoured in France

Buyouts (LBO/capital transmission): the dominant strategy

Buyouts (capital transmission / LBO)

represent the cornerstone of French private equity. A fund acquires a controlling (or otherwise significant) stake in

a profitable company, with a transformation agenda and a value creation plan.

According to the France Invest / EY study:

- 77% of value creation stems from EBITDA growth

- 36% from multiple expansion

- Leverage contribution is negative, at -13%

Value is therefore primarily driven by:

- organic growth,

- external growth (M&A),

- operational improvement.

Contrary to certain misconceptions, financial leverage is not the principal engine of performance: strategic and operational transformation of portfolio companies is the true source of alpha.

Growth equity: supporting corporate scaling

Growth equity and expansion capital support companies in their scaling phases. It finances already established businesses experiencing strong growth and seeking to change pace—through product development, international expansion, add-on acquisitions, or industrialisation—without necessarily pursuing a majority-control approach.

Innovative sectors—particularly cleantech and industrial technologies—attract significant capital.

Within the ecological transition:

- 71 fundraisings in H1 2025

- €1.26bn invested

- €528m allocated to renewable energy

Renewable energy accounts for more than 40% of invested amounts. French private equity therefore plays an active role in financing sustainable growth and industrial innovation.

Private debt and infrastructure: rapidly expanding strategies

Private debt

complements equity strategies and finances the economy outside traditional banking channels: unitranche, mezzanine,

senior, sponsor-backed financings, special situations, etc. It appeals to investors seeking a potentially more

“contractual” form of return (coupon) and stronger protections (security, covenants), while remaining exposed to

default risk and illiquidity.

In 2024:

- €11.6bn invested

- 276 transactions

- 53% of transactions incorporating ESG indicators

Private debt enables companies to access flexible financing that complements equity.

Infrastructure funds invest in long-duration assets (renewables, networks, mobility, digital infrastructure, etc.).

Infrastructure funds raised €13.7bn in 2024 (+16%), representing a 16% year-on-year increase. Energy and digital infrastructure lie at the heart of European strategic sovereignty priorities.

Leading private equity players in France

Reference French asset managers

The market comprises more than 380 asset managers that are members of France Invest.

Without aiming for exhaustiveness, several emblematic players illustrate the dynamism and international reach of French private equity:

- Ardian, one of the world’s leading private equity firms

- Tikehau Capital, a listed multi-strategy platform

- PAI Partners, a European buyout reference manager

Institutional investors and the gradual opening to private wealth investors

Historically, French private equity was built around an institutional investor base: insurers, pension funds, funds of funds, public institutions and banks. These stakeholders remain the backbone of the French market—both in terms of committed capital and allocation discipline.

According to France Invest, in the first half of 2025, funds of funds and institutional investors still represent a significant share of capital raisings, reflecting the enduring confidence of large allocators in the asset class.

Nonetheless, the French market has undergone a structural evolution over recent years: a progressive opening to private wealth investors, within a regulated and increasingly professionalised framework.

This trend is explained by several factors:

- The search for diversification beyond listed markets

- The pursuit of return in a more normalised rate environment

- Growing interest in the real economy and impact

- Improved structuring and distribution tools

This opening does not imply a commoditisation of French private equity. On the contrary, it is accompanied by:

- Heightened requirements in terms of education and transparency

- Rigorous selection of vehicles (FPCI, FCPR)

- Strict regulatory oversight

- Rising expertise among distributors

Private wealth investors—entrepreneurs, executives, families—now benefit from structured access to French private equity, via dedicated platforms and solutions aligned with institutional standards.

Nevertheless, the allocation rationale remains unchanged: French private equity is a long-term asset class requiring discipline, diversification and a clear understanding of its risk profile.

The objective is therefore not mass-market access, but rather qualified access—enabling private wealth investors to integrate French private equity progressively within a coherent overall asset allocation.

The role of France Invest within the French ecosystem

France Invest plays a structuring role through:

- Standardisation of data (European Data Cooperative)

- Publication of performance research

- Economic impact analysis

- Strategic workstreams on sovereignty

The association contributes to the professionalisation and international visibility of the French market.

Private Corner selects leading strategies across buyout, growth, private debt and infrastructure.

Private equity investment vehicles in France

FPCI: the “professional private equity fund”

The FPCI is the preferred vehicle for professional or well-informed investors.

Key characteristics:

- Reserved for qualified investors

- High investment flexibility

- Access to equity, infrastructure and private debt strategies

It enables diversified exposure to French and European private market assets.

FCPR and other AMF-regulated vehicles

FCPRs (fonds communs de placement à risque) are long-standing private equity vehicles designed for retail distribution in France.

They allow for:

- Majority allocation to private assets

- A specific tax framework

- Access to diversified private equity strategies

These vehicles are authorised by the AMF, ensuring a robust and secure regulatory framework.

Regulatory and tax framework for private equity in France

The French framework is recognised for its stability:

- AMF regulation

- AIFM Directive

- Enhanced transparency requirements

Taxation varies depending on the vehicle (FPCI, FCPR) and the investor profile (individual vs corporate).

France's regulatory framework increasingly encourages individuals to invest in private markets, through vehicles that are more accessible than ever.

Typical target companies in French private equity

Preferred targets

As of end-2024:

- 76% of backed companies are French

- 76% are SMEs

- 23% are mid-sized companies (ETIs)

- 34% are startups

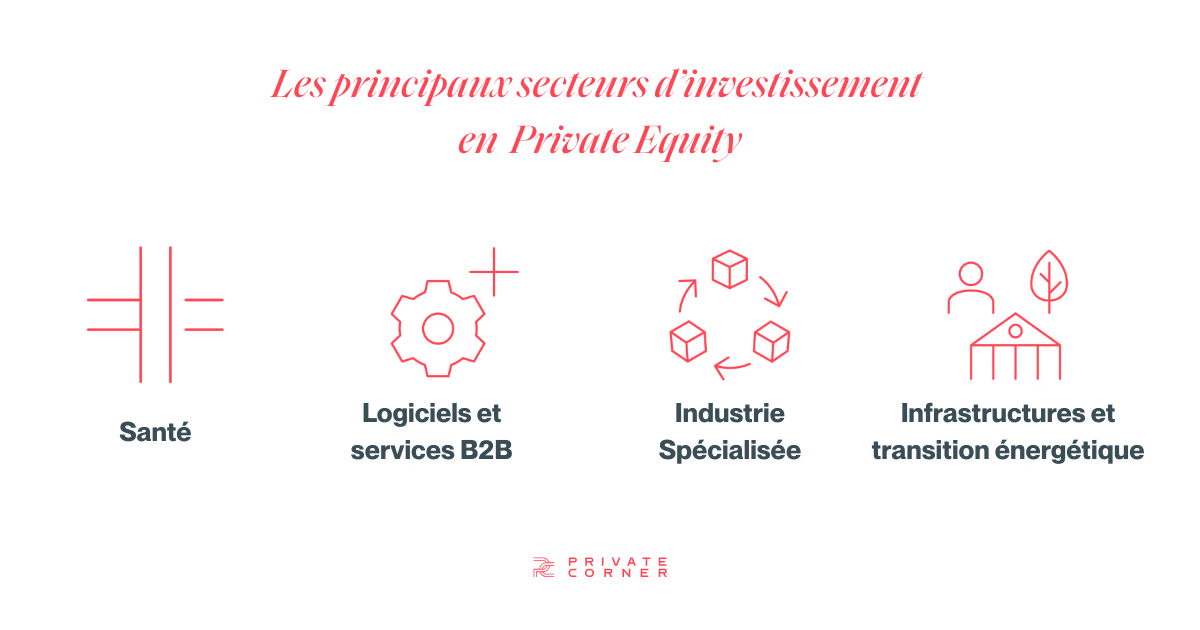

Key sectors

In France, the most dynamic sectors include:

- Healthcare (the leading private debt sector in 2024)

- Renewable energy

- Industry and B2B services

- Energy infrastructure

Healthcare, energy and industry increasingly concentrate invested capital, reflecting a strategic orientation towards assets with strong economic impact.

Private Corner provides independent financial advisers, private banks and family offices with a secure digital platform dedicated to private market assets.

Accessing French private equity with Private Corner

Accessing private equity in France presupposes rigorous manager selection, disciplined diversification and a nuanced understanding of market dynamics. In an asset class characterised by meaningful performance dispersion, access alone is insufficient: the structuring of commitments is decisive.

Private Corner enables independent advisers, private banks and family offices to access French private equity under conditions aligned with institutional standards—combining rigorous manager selection, strategy-level diversification and disciplined pacing of commitments over time.

How to select leading French managers and funds

Private Corner selects recognised asset managers across all segments:

- Private equity: buyout, growth, secondaries, co-investments, GP Stakes

- Private debt

- Infrastructure

The objective: replicate institutional best practices for intermediated private wealth investors.

Why invest in French growth companies?

French private equity primarily finances high-potential French SMEs and mid-sized businesses. As of end-2024, 76% of backed companies are headquartered in France.

Investing through French private equity funds provides indirect exposure to:

- Strategic industrial companies

- Healthcare operators

- Renewable energy projects

- Essential infrastructure assets

This exposure offers a direct participation in the growth of France’s real economy.

What support for intermediated private wealth investors?

Constructing a private equity allocation typically entails:

- Vintage-year diversification

- Progressive commitment pacing

- Cash-flow modelling

- Integration of specific risks (illiquidity, dispersion, leverage)

Private Corner supports financial advisers so they can incorporate private market assets coherently within their clients’ overall portfolios.

An institutional approach adapted to private wealth

Private Corner’s ambition is clear: enable wealth professionals to access French private equity on conditions comparable to institutional investors.

This implies:

- Rigorous selection standards

- Transparent disclosure of risks

- Appropriate investor education

- A secure digital platform

- A disciplined long-term approach

In a market where French private equity is attracting increasing amounts of capital, the ability to build a coherent allocation becomes a key differentiating factor.

Risks associated with private equity in France

Investing in French private equity entails specific risks that professional investors must incorporate into their allocation analysis.

- Illiquidity risk: funds are generally closed-ended for 8 to 12 years. Early exit options are limited.

- Capital loss risk: invested capital is not guaranteed. Performance depends on the manager’s ability to create value.

- Valuation risk: private assets are valued periodically using financial methodologies; valuations may move up or down.

- Macroeconomic and sector risk: portfolio companies may be affected by economic cycles or regulatory changes.

- Performance dispersion risk: dispersion between top and bottom quartiles remains material; manager selection is decisive.

- Leverage risk: in buyout strategies, debt can amplify outcomes both positively and negatively.

Disclaimer

Private Corner is authorised as a portfolio management company by the AMF on 05/11/2020 under number GP-20000038. Investing in private assets entails, among other risks, the risk of capital loss and illiquidity.

Sources for figures:

- France Invest & Grant Thornton — Activity of French private equity (H1 2025)

- France Invest & EY — Economic and social impact (as of end-2024)

- France Invest & EY — Net performance of private equity (as of end-2024)

- France Invest & EY — Value creation study (as of end-2024)

- France Invest, GreenUnivers & EY — Cleantech Barometer (H1 2025)

- France Invest & Deloitte — Activity of private debt funds (2024)

FAQ – Private equity in France

How large is the private equity market in France?

According to France Invest, private equity in France amounted to €36.9bn invested in 2024 (excluding infrastructure). The French market supports 11,142 portfolio companies and 2.5 million jobs.

Who are the main players in French private equity?

The French market includes more than 380 asset managers that are members of France Invest. These managers invest across:

- Venture capital & growth

- Expansion / development capital

- Buyout / capital transmission

- Private debt

- Infrastructure

Institutional investors (insurers, pension funds, funds of funds) remain the historical cornerstone of subscriptions. Since the 2019 Loi PACTE, private assets have progressively opened to private wealth investors.

What is an FPCI?

An FPCI (Fonds Professionnel de Capital-Investissement) is a regulated vehicle reserved for qualified investors. It provides exposure to private assets and is among the preferred structures for accessing institutional-grade private equity.

How can one invest in private equity in France?

For intermediated private investors, exposure to French private equity can be obtained via vehicles such as FPCI, FCPR, FIPS, FPS, etc. This can be implemented through a securities account, in registered form (nominatif pur), or via Luxembourg life insurance. For French life insurance and retirement savings plans (PER), insurers typically reference only liquid or evergreen funds.

For advisers, private banks and family offices, access usually requires:

- Rigorous asset manager selection

- Vintage-year diversification

- Progressive commitment pacing

- A thorough assessment of risks

Manager selection is decisive given the dispersion of performance.

Why include French private equity within a wealth allocation?

French private equity can provide:

- Diversification beyond listed markets

- Participation in the growth of French companies

- Historically attractive performance (12.4% net over 10 years)

- Tangible economic impact

It is a strategic lever for intermediated private wealth investors seeking long-term exposure to the real economy.