A private-assets allocation refers to the way a portfolio is split across assets not listed on a stock exchange, such as:

- Private Equity (buyouts, growth capital, secondaries).

- Private Debt (loans to unlisted companies).

- Infrastructure (energy, transport, telecoms).

- Unlisted Real Estate (offices, housing, warehouses).

This asset class allows investors to diversify their portfolio, access exclusive opportunities and benefit from returns potentially higher than those of traditional markets, in exchange for a risk of capital loss and lower liquidity.

💡 Good to know: It is common practice to recommend introducing between 5% and 20% of private assets into an overall allocation, depending on the investor's personal circumstances, projects and asset base. This range makes it possible to balance diversification, liquidity and exposure to high-potential themes, while tailoring the allocation to the objectives and constraints of each investor.

Investing in private markets has gradually established itself as a fully fledged component of wealth allocations. Long reserved for institutional investors, it is now accessible to a broader private-client base thanks to the evolution of investment vehicles and distribution solutions.

That said, investing in private assets does not come down to selecting a single private equity fund in isolation. As with listed markets, the performance of a portfolio depends above all on how it is built.

An investor may have access to the best managers in the market and still obtain a disappointing result if the allocation is poorly structured. Conversely, a coherent combination of complementary strategies often makes it possible to navigate economic cycles more serenely while multiplying the sources of value creation.

This is precisely the objective of the so-called "core-satellite" approach, widely used by institutional investors, insurance companies and family offices.

Introduction

On listed markets, an investor can achieve significant diversification with just a few index funds. In private markets, the reality is different. Each strategy has its own characteristics:

- investment horizon;

- distribution pace;

- level of diversification;

- sensitivity to economic cycles;

- value-creation driver.

A US buyout fund does not behave like a secondaries fund. A private debt strategy does not generate the same cash flows as an infrastructure fund. A vehicle exposed to technology does not necessarily move at the same pace as a portfolio centred on transport infrastructure.

The question, therefore, is not only which fund to invest in. The real question is: how do you combine several strategies in order to obtain a coherent portfolio?

The core-satellite approach: the method favoured by institutional investors

The core-satellite approach consists of distinguishing two categories of strategy within a single allocation. The core of the portfolio is designed to provide visibility, resilience and diversification. The satellites complement this base with more specific growth drivers. This construction helps to avoid two common pitfalls:

- a portfolio that is too cautious, limiting its value-creation potential;

- a portfolio that is too aggressive, depending on a limited number of investment bets.

The objective is to strike a balance between stability and performance.

Why choose a core-satellite approach?

| Criterion | Core | Satellites | Combination |

|---|---|---|---|

| Stability | ⭐⭐⭐⭐⭐ | ⭐⭐ | ⭐⭐⭐⭐ |

| Return potential | ⭐⭐⭐ | ⭐⭐⭐⭐⭐ | ⭐⭐⭐⭐ |

| Diversification | ⭐⭐⭐ | ⭐⭐⭐⭐ | ⭐⭐⭐⭐⭐ |

| Resilience to cycles | ⭐⭐⭐⭐⭐ | ⭐⭐⭐ | ⭐⭐⭐⭐ |

| Cash-flow visibility | ⭐⭐⭐⭐ | ⭐⭐ | ⭐⭐⭐⭐ |

No single strategy ticks every box. Core strategies generally offer greater visibility but more moderate performance potential. Satellite strategies can generate more performance but often come with greater economic volatility. Combining the two makes it possible to obtain a more balanced portfolio.

The core of the portfolio: the foundations of the allocation

The core of the portfolio forms the basis of the wealth-building construction. It brings together strategies capable of providing a degree of stability while participating fully in value creation.

Private Equity Secondaries

The secondary market consists of acquiring fund interests or stakes in funds that are already invested. Unlike a primary fund, which begins a new investment cycle, secondaries provide access to portfolios that are already built and often more mature. This characteristic generally offers better visibility on the assets held and helps to reduce the effect of the J-curve. Secondaries are today one of the cornerstones of many institutional allocations.

Example: Private Corner Secondary Fund 2026 (Committed Advisors)

GP Stakes

GP Stakes strategies consist of investing in management firms rather than directly in the underlying companies. The investor thereby benefits indirectly from the revenues generated by the platforms: management fees, carried interest and growth in assets under management. This strategy often presents a particularly resilient profile thanks to the recurring nature of these revenues.

Example: Blue Owl GP Stakes Strategy

Private Debt

Private debt consists of financing companies through unlisted loans. Unlike traditional private equity, where value creation rests primarily on the future resale of a company, private debt generates regular income through interest payments. This strategy generally provides greater visibility and often plays a stabilising role within an allocation.

Example: Private Corner Credit Yield

Infrastructure

Infrastructure makes it possible to invest in essential assets such as roads, hospitals, energy networks or social infrastructure. These assets frequently benefit from revenues contracted over long periods and sometimes indexed to inflation. For this reason, infrastructure is often regarded as one of the most wealth-oriented asset classes within private markets.

Example: Meridiam Global Infrastructure Strategies

The satellites: the growth engines of the portfolio

Once the foundations are laid, the satellites make it possible to add complementary performance drivers. They are designed to capture the major long-term economic and geographic trends.

European Buyout

This strategy mainly targets European family-owned companies that have reached a key stage in their development. Value creation generally rests on operational improvement, external growth and internationalisation.

Example: Private Corner Wealth Buyout 2026 (Ardian)

US Buyout

The United States is the world's leading private equity market. This exposure provides access to a particularly dynamic economic fabric as well as to some of the most experienced managers in the sector.

Example: US MidCap Buyout Strategies (Neuberger Berman)

Asia ex-China

Asia is today one of the main engines of global economic growth. This strategy makes it possible to benefit from the development of services, the rise of the middle classes and the expansion of sectors such as healthcare and technology.

Example: Private Corner Buyout EQT Strategy

Technology & Healthcare

Technology and healthcare are among the most powerful structural trends in the global economy. Investing in these sectors makes it possible to support companies benefiting from growth dynamics that may extend over several decades.

Example: PC Feeder Keensight Nova VII

A concrete core-satellite allocation example

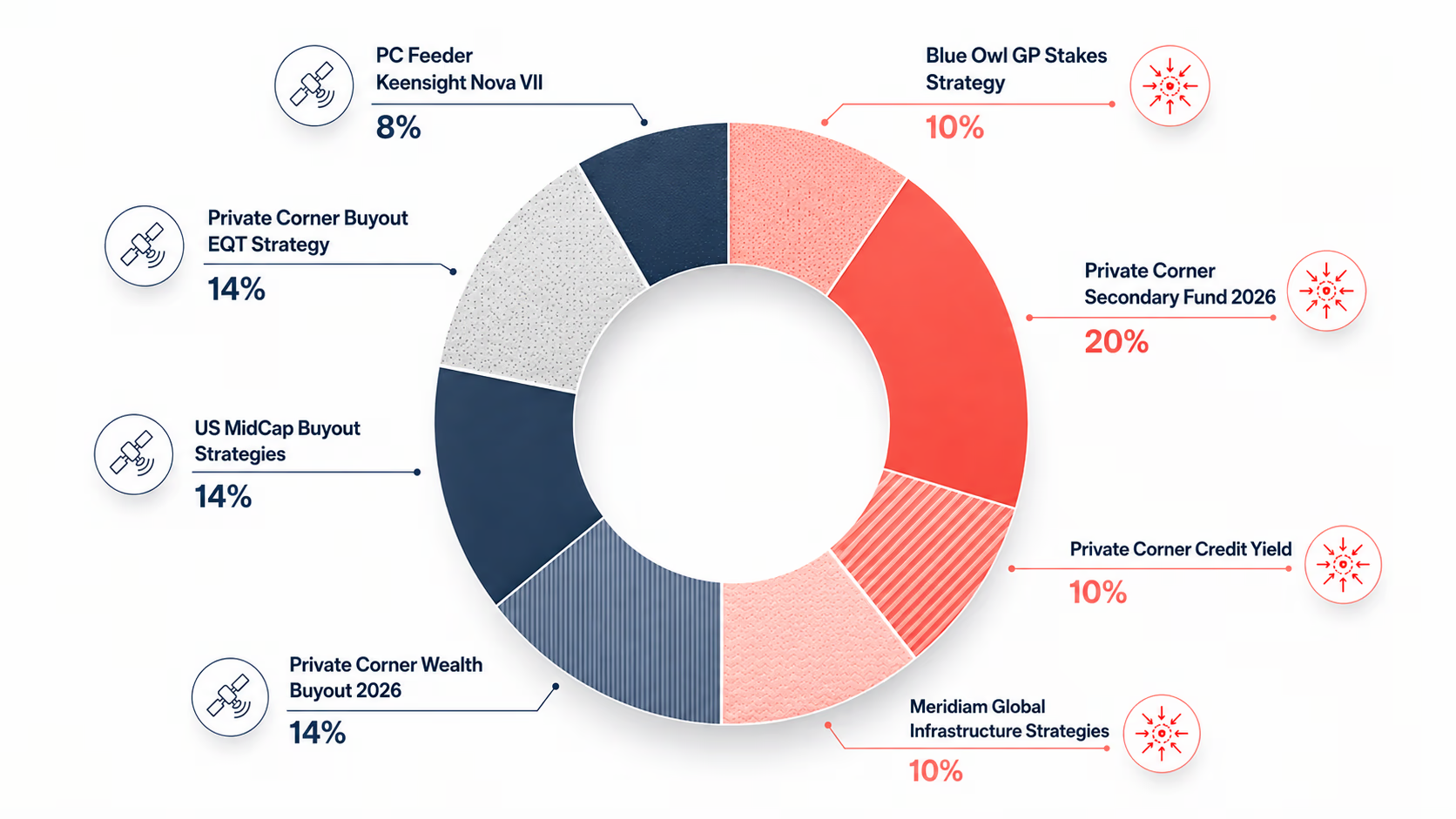

Take the case of an investor wishing to allocate 2.4 million euros to private assets. A balanced construction could take the following form:

Core of the portfolio (50%)

| Fund | Weight |

|---|---|

| Private Corner Secondary Fund 2026 (Committed Advisors) | 20% |

| Blue Owl GP Stakes Strategy (Blue Owl) | 10% |

| Private Corner Credit Yield (CVC + General Atlantic) | 10% |

| Meridiam Global Infrastructure Strategies (Meridiam) | 10% |

Satellites (50%)

| Fund | Weight |

|---|---|

| Private Corner Wealth Buyout 2026 (Ardian) | 14% |

| US MidCap Buyout Strategies (Neuberger Berman) | 14% |

| Private Corner Buyout EQT Strategy (EQT) | 14% |

| PC Feeder Keensight Nova VII (Keensight Capital) | 8% |

This breakdown aims to combine strategies offering visibility and resilience with more specific growth drivers. It is presented purely for illustrative purposes and constitutes neither investment advice nor a personalised recommendation.

⚠️ Warning: investing in private assets entails a risk of capital loss, illiquidity over several years and possible dispersion of performance between funds. Past performance is not a reliable indicator of future performance. Any allocation must be tailored to the wealth situation, objectives and investment horizon of each investor.

Key takeaways

The success of a private-assets allocation rests less on the search for the perfect fund than on the ability to combine several complementary strategies.

The core-satellite approach makes it possible precisely to build a balanced portfolio by combining:

- a core of the portfolio made up of strategies that provide visibility, diversification and resilience;

- satellites that make it possible to capture the major long-term economic and geographic trends.

This methodology, widely used by institutional investors, is today one of the most relevant approaches for building durable exposure to private assets.

Access a selection of institutional funds and dedicated support.

FAQ

What share of one's wealth should be invested in private assets?

It is generally accepted that an allocation of between 5% and 20% of financial wealth can be a relevant starting point, subject to the investor's personal circumstances and investment horizon.

Why not invest solely in private equity buyout?

Because buyout represents only one source of value creation. Institutional investors generally seek to combine several performance drivers in order to reduce concentration risk.

Why include secondaries?

Secondaries often help to mitigate the J-curve, accelerate distributions and improve visibility on the underlying assets held.

How many funds should one hold?

There is no ideal number. The objective is above all to diversify performance drivers, geographies and management styles.

What are the risks of investing in private assets?

Investing in private assets entails a risk of capital loss, illiquidity over several years and potential dispersion of performance between funds. Past performance is not a reliable indicator of future performance. These characteristics justify a diversified approach and a long investment horizon.

Disclaimer

This document is provided for information purposes only and constitutes neither an offer to subscribe, nor a personalised recommendation, nor investment, legal or tax advice.

The information presented (investment strategies, sectors, geographies, taxation, minimum amounts, fundraising timelines and closing dates) is subject to change and may be modified at any time by the management companies.

Any investment in private equity, private debt, secondaries or infrastructure funds entails, in particular, a risk of partial or total loss of capital, a liquidity risk and requires a long-term investment horizon. Past performance is not a reliable indicator of future performance and management objectives do not constitute a guarantee of return.

Any investment decision must be taken after reviewing the regulatory documentation of the fund concerned and assessing its suitability in light of the investor's situation, objectives, investment horizon and ability to bear the associated risks.