To hear some market commentators tell it, the verdict seems clear: private equity is going through a rough patch. Fundraising is slowing, exits are taking longer, and investors are becoming more selective in their commitments. Yet the data tells a different story.

The Global Private Equity Report 2026 published by Bain & Company shows that the private markets industry is not dead — it is simply changing the rules of the game. After more than a decade driven by exceptionally favourable financial conditions, the sector is entering a phase where performance depends less on the macroeconomic backdrop and more on fund managers' ability to create value. In other words, the sector may not be in crisis. It is coming of age.

A rigorous selection of institutional managers, available to wealth management professionals.

Activity levels that remain historically high

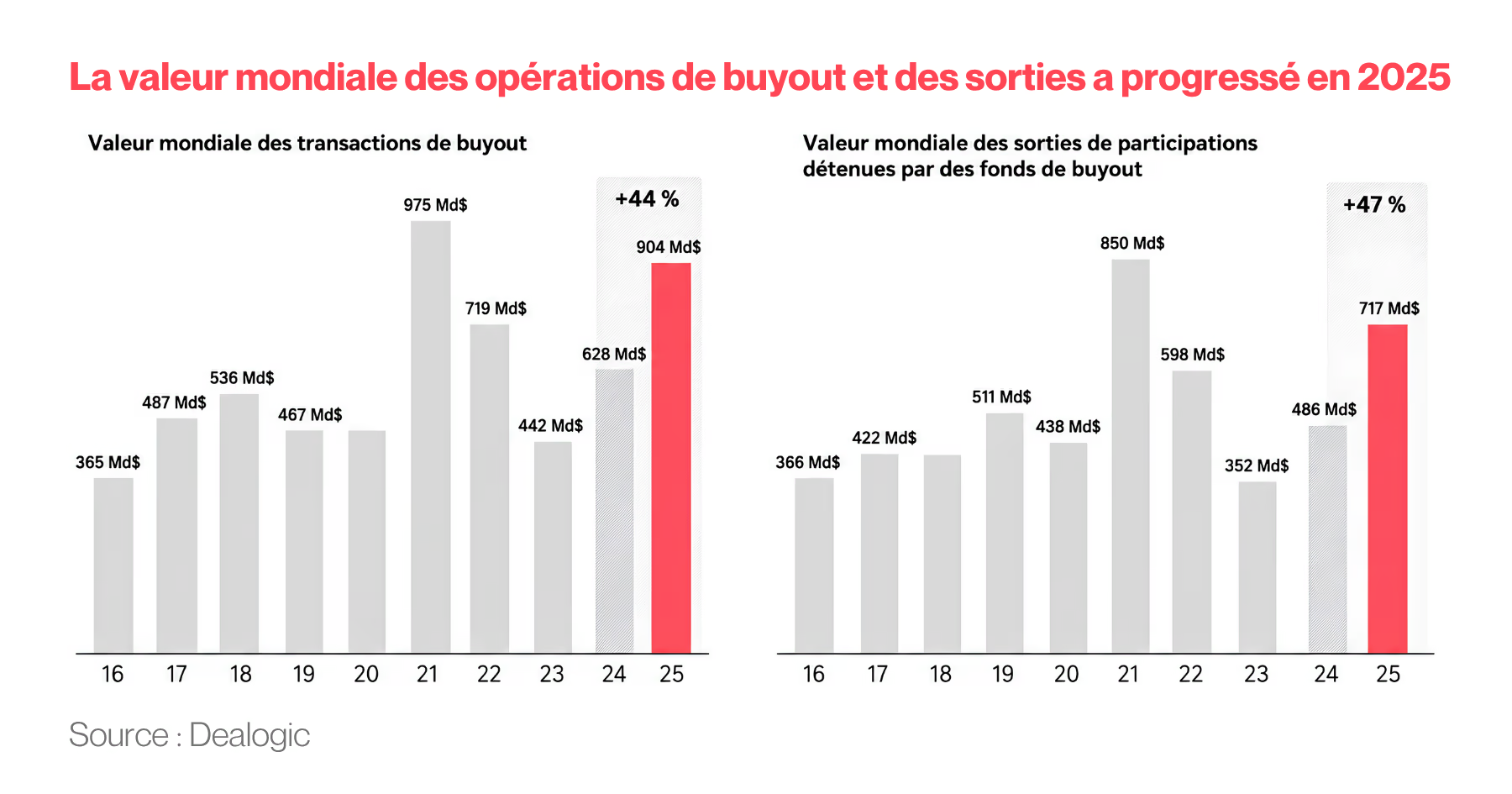

The 2025 figures are hard to reconcile with the idea of an industry in crisis:

- $904 billion invested (+44% versus the prior year)

- $717 billion in exits (+47%)

According to Bain, this marks the second-highest level of activity ever recorded in private equity, surpassed only by 2021 — itself an exceptional year by many measures.

These figures show that transactions continue to close at a sustained pace. The market has not recaptured the exuberance of the zero-rate era, but it remains extremely active on a global scale.

The reality, then, is less one of structural slowdown and more one of a return to more normal conditions.

The real challenge: restoring the liquidity cycle

The primary challenge facing the industry today is less about investment activity and more about liquidity.

For several years, exits have been held back by rising interest rates, financial market volatility, and valuation gaps between buyers and sellers. This has reduced distributions to investors, mechanically limiting their ability to redeploy capital into new funds.

The dynamic has created a relatively straightforward chain:

- fewer exits;

- fewer distributions;

- fewer new commitments.

Against this backdrop, the 47% increase in exits recorded in 2025 is a particularly significant signal. It suggests the market is gradually returning to smoother functioning.

Many market participants expect this improvement to continue in the coming years, driven by a progressive reopening of capital markets, the development of the secondary market, and a recovery in M&A activity.

A substantial backlog of assets awaiting exit

One of the most striking figures in the report concerns the volume of companies currently held by funds.

Nearly 32,000 companies remain in portfolio today, representing an estimated value of approximately $3.8 trillion.

This situation can be read in two ways. Pessimists see a market bottleneck and growing pressure on managers to complete disposals. Optimists, on the other hand, see a large reservoir of future transactions. As financing conditions stabilise and valuations normalise, a meaningful share of these assets could return to market.

In other words, this backlog of portfolio companies is potentially a significant source of activity for years to come.

Private Corner offers an institutional selection of private equity, private debt, and infrastructure funds.

The end of an exceptional cycle

But the most important message in the report concerns neither invested volumes nor exit prospects. It concerns the very nature of future performance.

For nearly fifteen years, private equity benefited from a particularly favourable environment:

- historically low interest rates;

- abundant and cheap debt;

- strong expansion of valuation multiples;

- ample market liquidity.

In that context, a significant portion of returns came naturally from favourable macroeconomic tailwinds. Investors were riding a powerful wave.

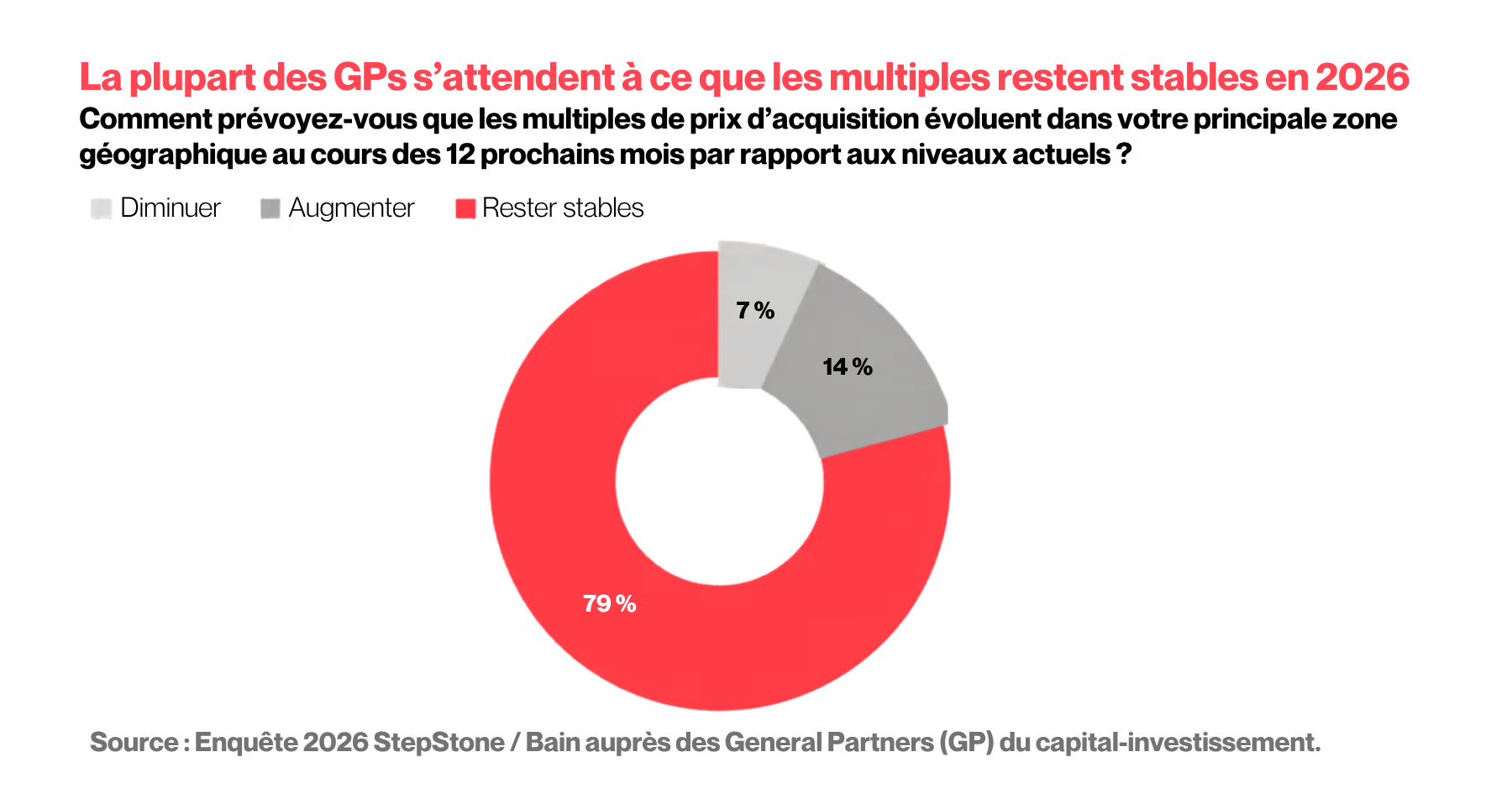

Today, that tailwind has largely faded. Financing costs are higher, multiples are expanding more slowly, and investors have grown more demanding. Value creation must therefore come increasingly from factors that managers can directly control.

"12 is the new 5"

Bain summarises this new reality with a deliberately simple formula: "12 is the new 5".

For many years, a fund could buy a company at 5x EBITDA and sell it a few years later at 12x EBITDA. A significant share of performance came from multiple expansion, driven by low rates, abundant debt, and seller-friendly markets.

Today, in many sectors, companies are already being acquired at around 12x EBITDA. If you buy at 12x and sell at 12x, the market no longer generates performance on your behalf.

The only way to create value is then to improve the company itself: accelerating revenue growth, strengthening profitability, improving margins through operational transformation, pursuing add-on acquisitions, or expanding into new markets. In short, private equity is returning to its fundamentals — creating value before monetising it. The industry has entered a phase where buying well and riding a favourable market is no longer enough.

Financial leverage remains an important tool, but it is no longer a sufficient performance driver on its own.

A more mature and more selective industry

At its core, Bain is not describing an industry in trouble. It is describing an industry reaching maturity.

As is often the case in fast-growing sectors, the early years were largely supported by an exceptionally favourable environment. The current phase is different: it demands more discipline, more operational expertise, and more rigorous investment selection.

This shift could even widen the gap between top-tier managers and the rest of the market. When conditions become more demanding, the quality of execution takes on growing importance. Teams capable of identifying the right companies, supporting their transformation, and genuinely creating operational value should continue to stand out.

The real debate is no longer about private equity's survival

The question is probably no longer whether private equity still works. The figures show the industry remains dynamic, capital continues to be deployed, and exits are gradually picking up.

The real challenge now lies elsewhere. It consists in identifying the managers capable of generating returns in an environment where leverage, falling rates, and multiple expansion no longer do the work for them. In this new cycle, manager selection, execution quality, and operational value creation are once again decisive. The gap between the best market participants and the rest is likely to widen further than it did over the past decade.

Private equity is not entering a phase of decline. It is entering a phase of higher standards. And it is often in the most demanding markets that the best investors truly demonstrate their skill.

Private Corner analyses and lists the best institutional funds for wealth management professionals.